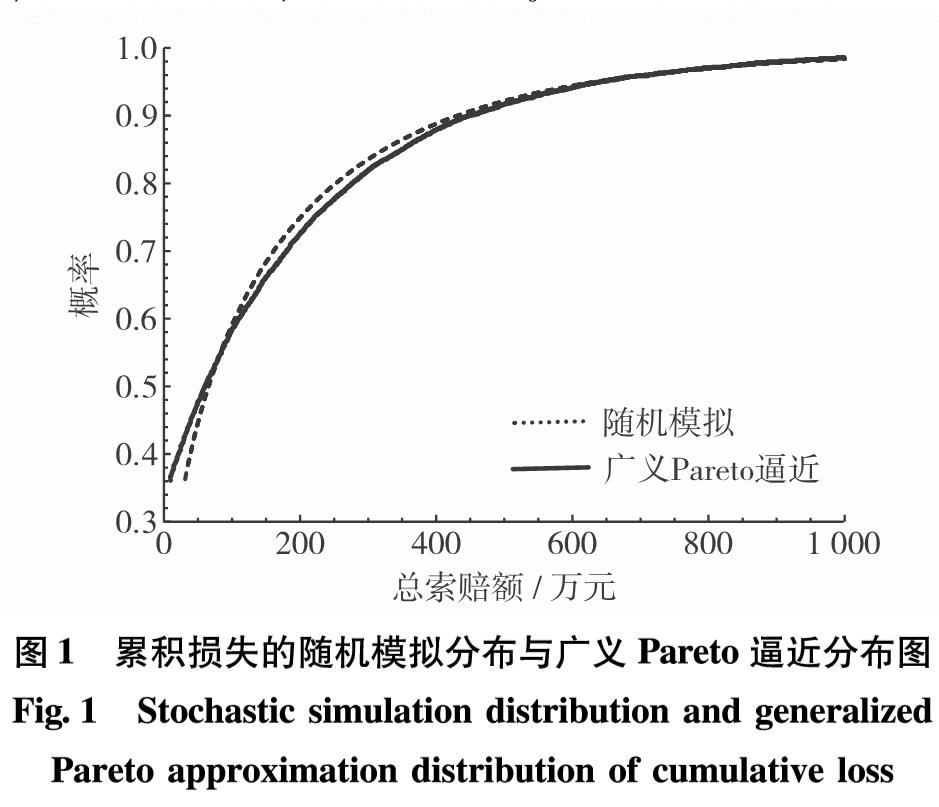

令个体索赔额X(单位:万元)服从Pareto型重尾分布

FX(x)=1-(300/(300+x))4, x>0.

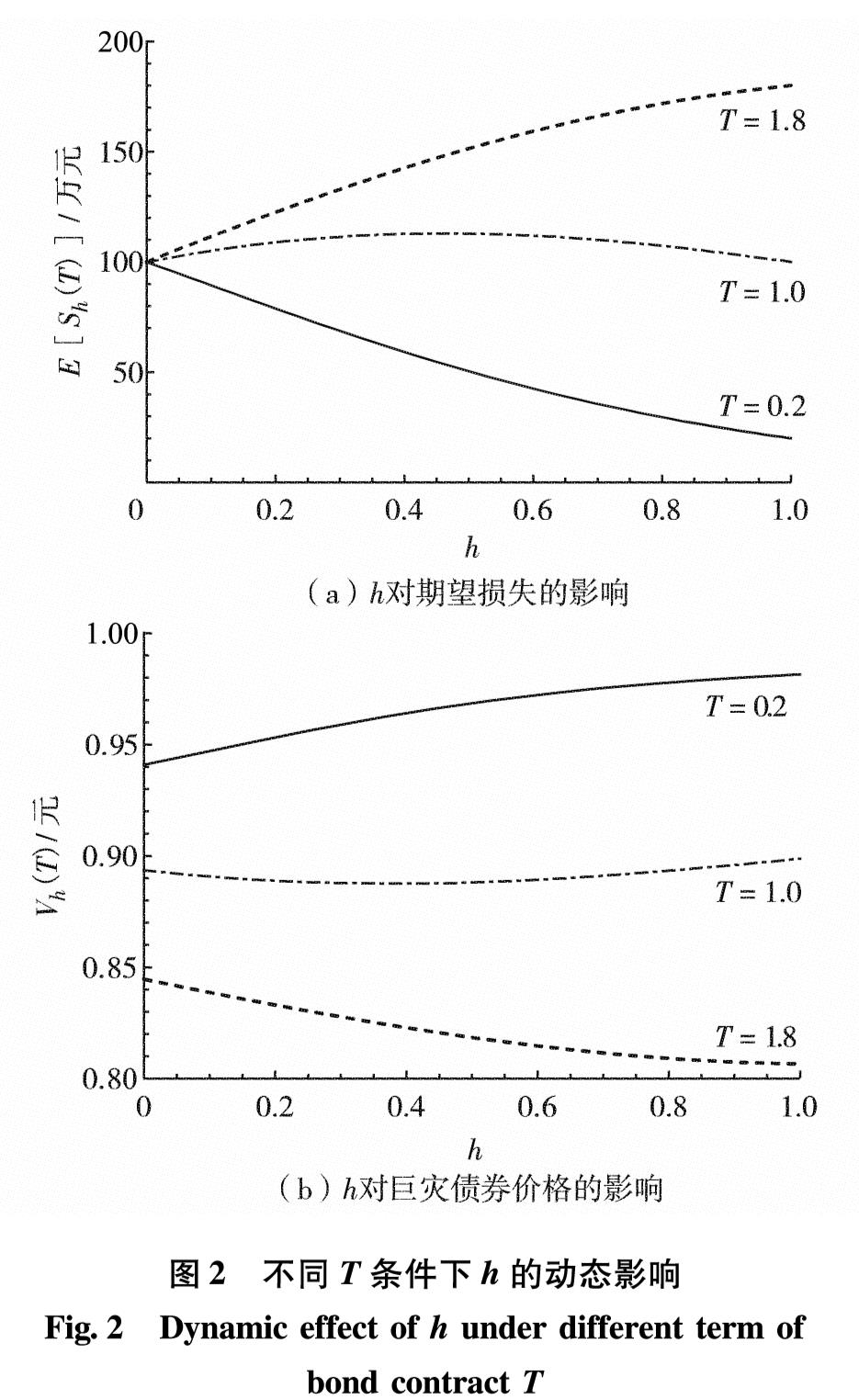

给定λ=1, T=2及h=0.5, 对累积索赔Sh(T)的分布进行随机模拟(其中,分数Poisson过程的模拟方法可

参考文献[28]),并与逼近分布FS进行比较,结果如图1.

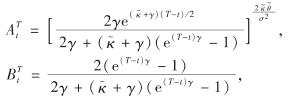

图1 累积损失的随机模拟分布与广义Pareto逼近分布图

Fig.1 Stochastic simulation distribution and generalized Pareto approximation distribution of cumulative loss

由图1可见,定理1所给出的逼近效果良好,特别是对大额索赔拟合程度非常高,这与本研究更关注巨灾索赔厚尾特性的考虑相一致.

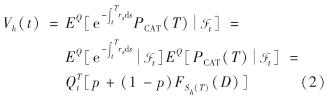

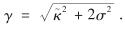

给定利率模型相关参数κ=0.20, θ=0.10, λr=-0.01, σr=0.08, r0=0.06, 支付比例p=0.050, 市场风险参数λr=-0.01及门限水平D=300. 将期限水平T及记忆参数h∈(0,1]视作变量,考察不同期限水平下,记忆参数对期望风险和债券价格的动态影响,结果如图2.

由图2(b)可知,债券合约的期限T越长,债券价格越低,因为利率风险增多且触发条件发生的巨灾风险也越大(门限水平固定).进一步对比图2(b)与图2(a)发现,对给定的期限T, 随着记忆参数的增大,债券价格出现单调递增(T=0.2)、 先减后增(T=1.0)及单调递减(T=1.8)多种情形,并无确定的变化趋势,且与期望损失的变化情形正好相反.这符合风险与收益成正比的均衡原则,因为期望损失越大,投资者面临的风险增大,债券价格下降,期望收益提高.至于记忆参数增大的条件下,期望损失及债券价格均没有确定变化趋势的现象,主要与索赔次数有关.实际上,Mittag-Leffer型等待时间变量具有重尾特性,记忆参数h的增大可能引起索赔次数期望值的递增或递减.与传统指数型索赔等待时间不同,Mittag-Leffer型等待时间具有无穷均值.

图2 不同T条件下h的动态影响

Fig.2 Dynamic effect of h under different term of bond contract T

结 语

中国是世界上受自然灾害影响最严重的几个国家之一,尽快建立合理的巨灾保险制度具有重要意义.目前,中国巨灾保险试点工作不断推进,但仍需进一步创新产品设计开发,建立多层次巨灾风险分散机制.本研究为了准确评估承保巨灾风险可能给保险公司带来的冲击,采用更贴近保险实务的复合分数Poisson模型刻画保险公司的风险过程,并考虑巨灾风险的厚尾特征,运用广义Pareto型逼近分布; 为合理分散和转移巨额损失,研究了CIR利率模型下巨灾保险连接债券的定价问题,并给出相应定价公式.结合数值示例验证分布逼近的有效性,其对高额索赔的拟合效果理想.在不同债券期限水平下,考察记忆参数对期望风险和债券价格的影响.结果表明,记忆参数的增大对期望风险和债券价格的影响呈现出相反而多形态的趋势,与期限水平密切相关.研究说明了单调性相反的现实意义,多形态趋势的原因主要与记忆参数对期望索赔次数的影响有关.然而,该影响机制的更深层次原因还有待进一步探究,可能与记忆效应的长期和短期性有关.鉴于Mittag-Leffer分布的特殊性及其非初等密度函数处理的非平凡性,要探明其确切原因还需要一些处理技术的突破,这将作为下一步研究的重要方向.

即参数为h的分数Poisson过程. {Xi: i≥1}与Nh(t)独立时,称模型(1)为复合分数Poisson模型.

即参数为h的分数Poisson过程. {Xi: i≥1}与Nh(t)独立时,称模型(1)为复合分数Poisson模型.

为波动率.

为波动率.

仍为一个标准布朗运动, 且

仍为一个标准布朗运动, 且 为确定利率风险的市场价格参数, 通常λr<0.

为确定利率风险的市场价格参数, 通常λr<0.

,

,

,0<x<1,参数a>0, b>0.

,0<x<1,参数a>0, b>0.

, 表示X的特征函数.将

, 表示X的特征函数.将 对z求导可得

对z求导可得

对z求导可得

对z求导可得