离散时间期限结构模型主要研究直接模拟利率和模拟零息债券的演化.本文重点讨论后者.

1.1 二叉树市道轮换期限结构模型的框架

考虑建立在概率空间(Ω, F, P)上的1个离散时间金融市场.假设金融交易只能发生在固定的时间0,1,2,…,T*, 记T={0,1,…,T*}. 对于有限数m,定义集合E={1,2,…,m}. 假设概率空间上有一对取值于E×N的过程(Xn,Tn),(Xn,Tn)是半马氏核Q的齐次马氏更新过程,即对所有的n,Xn,j和t, 有

P(Xn+1=j; Tn+1-Tn≤t|X0,T0,…,Xn,Tn)=

P(Xn+1=j; Tn+1-Tn≤t|Xn)=QXn j(t).

定义vt=maxn{Tn≤t}, 则核Q的半马氏过程定义为Yt=Xvt. 假设Y0是已知非随机的,随机过程Y将控制经济的状态.过程Kt定义为Kt=t-[sup{k<t:Yk≠Yt}+1], 表示从最后一次状态跳跃时刻到现在时刻t之间的时间.假设K0是已知非随机的,过程Kt是半马氏过程的后向回复时间过程(可

参考文献[18]).最后,定义Ft=σ(ζs, Ys, Ks, 0≤s≤t), ζs定义为向上游走或向下游走的倍数过程.

定义一个到期日为T≤T*的零息债券是在到期日T产生一单位货币的金融产品.用τ表示t时刻距离零息债券到期日的时间,即τ=T-t. 记Pt(τ)为t时刻距离到期日时间为τ的零息债券的价格.假设给定一个初始期限结构,即对所有的τ, 给定Pt(τ)的一组值.对任意的τ和状态i∈E, 假设存在两个实值ui(τ)和di(τ), ui(τ)和di(τ)都是严格为正的,且ui(τ)>di(τ). 记ui=(ui(1),ui(2), …, ui(T*)), di=(di(1), di(2), …, di(T*)). 引入规模为T*的一个随机过程ζt, 规定P(ζt+1=uYt|Ft)=1-P(ζt+1=dYt|Ft), uYt和dYt分别为Yt状态下向上和向下游走的倍数. 该过程描述了从t时刻到t+1时刻期限结构的演化,若ζt+1=uYt, 称期限结构向上移动,若ζt+1=dYt, 则称期限结构向下移动,假设在给定Ft的条件下, ζt+1与Yt+1是条件独立的,即对于任意的t≥1, P(ζt+1=uYt, Yt+1=j|Ft)=P(ζt+1=uYt|Ft)P(Yt+1=j|Ft). 记 P(Yt+1=j|Ft)=v jt, 根据过程Y的结构, 有vtj=P(Yt+1=j|Yt, Kt).

定理1 概率vjt是一个“带有初始后向轮换概率”的特殊情形

vjt={(QYt j(Kt+1)-QYt j(Kt))/(1-∑mj=1QYt j(Kt)), j≠Yt

(1-∑mj=1QYt j(Kt+1))/(1-∑mj=1QYt j(Kt)), j=Yt

【证】记qij(t)=P(Xn+1=j, Tn+1-Tn=t|Xn)=i, 则Qij(t)=P(Xn+1=j, Tn+1-Tn≤t|Xn=i)=∑tk=0qij(k)为半马氏核; Hi(t)=P(Tn+1-Tn≤t|Xn=i)=∑mj=1Qij(t)为过程在状态i逗留时间的分布函数; Ψij(t)=∑tk=0P(Xk=j,Tk=t|X0=i)为时刻0从状态i出发,半马氏链在时刻t跳跃到状态j的概率; Ψ·j(t)=∑i∈EΨij(t)=∑tk=0P(Xk=j, Tk=t)为半马氏链在时刻t跳跃到状态j的概率;

Pi(Yt=j, Kt)=P(Yt=j, Kt|Y0=i, K0=0)=∑t-Ktn=0P(Xn=j, Tn=t-Kt,Tn+1>t|X0=i)=

∑t-Ktn=0P(Tn+1-Tn>Kt|Xn=j)P(Xn=j, Tn=t-Kt|X0=i)=

[1-Hj(Kt)]∑t-Ktn=0P(Xn=j, Tn=t-Kt|X0=i)=[1-Hj(Kt)]Ψij(t-Kt).

P(Yt=j, Kt)=[1-Hj(Kt)]Ψ·j(t-Kt).

若下一个交易时刻经济状态发生跳跃,即j≠Yt, 则

v jt=P(Yt+1=j, Kt+1=0|Yt, Kt)=(P(Yt+1=j, Kt+1=0, Yt, Kt))/(P(Yt, Kt))=

(∑t-Ktn=0P(Tn+1=t+1, Xn+1=j, Tn=t-Kt, Xn=Yt))/(P(Yt, Kt))=

(∑t-Ktn=0P(Tn+1=t+1, Xn+1=j|Tn=t-Kt, Xn=Yt)P(Tn=t-Kt, Xn=Yt))/(P(Yt, Kt))=

(qij(Kt+1)∑t-Ktn=0P(Tn=t-Kt, Xn=Yt))/([1-HYt(Kt)]Ψ·Yt(t-Kt))=(qij(Kt+1))/(1-HYt(Kt))=(Qij(Kt+1)-Qij(Kt))/(1-∑mj=1Qij(Kt)).

若下一个交易时刻经济状态没有发生跳跃,即j=Yt, 则

v jt=P(Yt+1=Yt, Kt+1=Kt+1|Yt, Kt)=(P(Yt+1=Yt, Kt+1=Kt+1, Yt, Kt))/(P(Yt, Kt))=

(∑Yt+1∈E∑t-Ktn=0P(Tn+1>t+1, Xn+1=Yt+1, Tn=t-Kt, Xn=Yt))/(P(Yt, Kt))=

(∑t-Ktn=0P(Tn+1>t+1|Tn=t-Kt, Xn=Yt)P(Tn=t-Kt, Xn=Yt))/(P(Yt, Kt))=

(∑t-Ktn=0P(Tn+1-Tn>Kt+1|Xn=Yt)P(Tn=t-Kt, Xn=Yt))/(P(Yt, Kt))=

([1-HYt(Kt+1)]∑t-Ktn=0P(Tn=t-Kt, Xn=Yt))/([1-HYt(Kt)]Ψ·Yt(t-Kt))=(1-HYt(Kt+1))/(1-HYt(Kt))=(1-∑mj=1QYt j(Kt+1))/(1-∑mj=1QYt j(Kt)).

定义P(ζt+1=uYt|Ft)=zt, 显然πjt:=P(ζt+1=uYt, Yt+1=j|Ft)=ztvjt, 进而kjt:=P(ζt+1=dYt, Yt+1=j|Ft)=(1-zt)vjt. 因此, 对于t, 有∑mj=1(πjt+kjt)=1.

当给定Ft, 一对过程Y和K在t+1时刻可以取m个不同的值.事实上,假设Yt=i, Kt=k, 则(Yt+1, Kt+1)=(i, k+1), 或者对于任意的j≠i,(Yt+1, Kt+1)=(j, 0). 然而,由过程ζ, Y和K组成的系统可以取2m个不同的值,这些值都由下面的事件集确定(可作为事件Aj,ut+1和Aj,dt+1的定义): Aj,ut+1={ω∈Ω:Yt+1=j, ζt+1=uYt}; Aj,dt+1={ω∈Ω:Yt+1=j, ζt+1=dYt}.

1.2 Ho-Lee模型的拓展

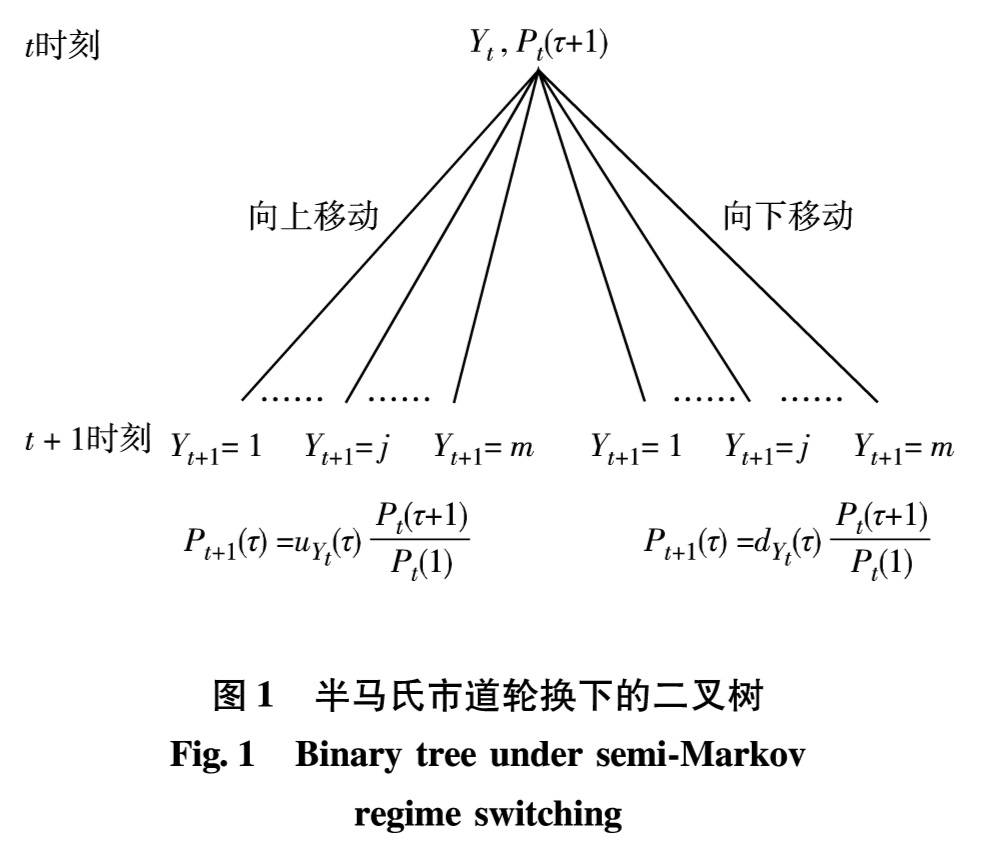

经典Ho-Lee模型解决了零息债券的动态性,本研究将Ho-Lee模型拓展至包括模型参数转变的情形.给定Ft, 期限结构的演变如图1. 对于所有的τ, 在Aj,ut+1上,有Pt+1(τ)=uYt(τ)(Pt(τ+1))/(Pt(1)); 在Aj,dt+1上,有Pt+1(τ)=dYt(τ)(Pt(τ+1))/(Pt(1)).

图1 半马氏市道轮换下的二叉树

Fig.1 Binary tree under semi-Markov regime switching

这里可以写为Pt+1(τ)=uYt(τ)(Pt(τ+1))/(Pt(1))(∑mj=1IAj,ut+1)+dYt(τ)(Pt(τ+1))/(Pt(1))(∑mj=1IAj,dt+1).使用先前的记号,有P[Pt+1(τ)=uYt(τ)(Pt(τ+1))/(Pt(1))|Ft]=zt; P[Pt+1(τ)=dYt(τ)(Pt(τ+1))/(Pt(1))|Ft]=1-zt.进而(假设这些概率都严格为正)P[Pt+1(τ)=uYt(τ)(Pt(τ+1))/(Pt(1)); Yt+1=j|Ft]=πjt, P[Pt+1(τ)=dYt(τ)(Pt(τ+1))/(Pt(1)); Yt+1=j|Ft]=kjt.

假设事件Ai,u和Aj,u(或Ai,d和Aj,d)发生时,零息债券的价格相同,即当期限结构向上(或向下)移动时,无论是否有市道轮换,下一个时期零息债券的价格均为 Pt+1(τ)=uYt(τ)(Pt(τ+1))/(Pt(1))(或Pt+1(τ)=dYt(τ)(Pt(τ+1))/(Pt(1))). 这说明市道轮换的影响只体现在下一个时期.

1.3 无套利框架下的利率结构

套利策略是指在没有风险、没有初始投资的情况下得到确定利润的策略.市场上没有套利策略称为无套利条件.下面证明无套利意味着模型参数满足一些条件.

引理1 无套利表明,对于每个τ和i∈E, ui(τ)>1>di(τ).

定理2 无套利意味着满足下列条件的过程pt存在:

对于每个t, 0<pt<1; 对于所有的τ, ptuYt(τ)+(1-pt)dYt(τ)=1.

【证】 考虑1个单期模型.假设给定零息债券价格Pt(·)的结构,构建一个投资组合:包含1个到期日为T+1的零息债券(距离到期日的时间为τ+1)和H个到期日为T″+1的零息债券(距离到期日的时间为τ″+1).

在时刻t, 投资组合的价值为W(t)=Pt(τ+1)+HPt(τ″+1).

在时刻t+1, 根据本研究建立的模型,投资组合能且只能取2个值.

在集合∪j∈EAj,ut+1上,有W(t+1)=uYt(τ)(Pt(τ+1))/(Pt(1))+HuYt(τ″)(Pt(τ″+1))/(Pt(1));

在集合∪j∈EAj,dt+1上,有W(t+1)=dYt(τ)(Pt(τ+1))/(Pt(1))+HdYt(τ″)(Pt(τ″+1))/(Pt(1)).

现选取一个H使其满足无论哪个事件发生,投资组合的值都是相同的.这意味着投资组合在这段时间内实际上是无风险资产,因此,这个投资组合应该与到期日为T+1的零息债券有相同的回报,由此引出2个条件

uYt(τ)Pt(τ+1)+HuYt(τ″)Pt(τ″+1)=

dYt(τ)Pt(τ+1)+HdYt(τ″)Pt(τ″+1)(1)

W(t)=Pt(1)W(t+1)(2)

式(2)可改写为

Pt(τ+1)+HPt(τ″+1)=

dYt(τ)Pt(τ+1)+HdYt(τ″)Pt(τ″+1)(3)

由式(1)和式(3)具有相同的H值,故可得

((dYt(τ)-uYt(τ))Pt(τ+1))/((uYt(τ″)-dYt(τ″))Pt(τ″+1))=

((dYt(τ)-1)Pt(τ+1))/((1-dYt(τ″))Pt(τ″+1)),

即(dYt(τ)-uYt(τ))/(uYt(τ″)-dYt(τ″))=(dYt(τ)-1)/(1-dYt(τ″)), 所以(1-dYt(τ″))/(uYt(τ″)-dYt(τ″))=(1-dYt(τ))/(uYt(τ)-dYt(τ)). 因为τ和τ″是任意选择的,可以记(1-dYt(τ″))/(uYt(τ″)-dYt(τ″))=pYt:=pt. 显然, 0<pt<1. 进而得

ptuYt(τ″)+(1-pt)dYt(τ″)=1.(4)

除了概率过程pt随着时间变化,最后的结果与Ho-Lee模型相同.过程pt的取值依赖于Yt而不依赖于τ, 对于Yt的每个可能值都有ptuYt(τ)+(1-pt)dYt(τ)=1.

推论1

Pt(τ″+1)=Pt(1)[ptuYt(τ″)(Pt(τ″+1))/(Pt(1))+

(1-pt)dYt(τ″)(Pt(τ″+1))/(Pt(1))](5)

由此说明t时刻零息债券的价值仅仅是t+1时刻可能价值折现的平均.

1.4 最小熵鞅测度

在套利策略定义中,有关期望是在物理概率测度之下取得的,为建立鞅概率测度,需用到等价测度的概念.

引理2 对于任意的j∈E和t∈T, 定义一系列严格为正的参数(pjt, qjt)j∈E; t∈T, 且满足对于任意的t∈T, ∑mj=1(pjt+qjt)=1. 定义

Dt=∏t-1s=0(∑mj=1[(pjs)/(πjs)IAj,us+1+(qjs)/(kjs)IAj,ds+1])(6)

则对于所有的t, Dt>0, E[Dt]=1且 E[Dt+1|Ft]=Dt.

这些结论允许Dt可以作为一个密度过程,这个过程将被用于介绍等价测度.

定理3 定义P*是P的等价测度,密度为DT*. 假设对于所有的t, ∑mj=1pjt=pt,pt的定义如式(4),则测度 P*是1个等价鞅测度.

【证】 根据定义 P*是1个等价测度.但在这个测度下,每个债券是否表现为1个鞅还有待证明.

E*[Pt(1)Pt+1(τ)|Ft]=

1/(Dt)E[Pt(1)Pt+1(τ)Dt+1|Ft]=

Pt(τ+1)E[∑mj=1((uYt(τ)pjt)/(πjt)IAj,ut+1+

(dYt(τ)qjt)/(kjt)IAj,dt+1|Ft]=

Pt(τ+1)(uYt(τ)∑mj=1pjt+dYt(τ)∑mj=1qjt)

根据∑mj=1pjt=pt和定理2得 E*[Pt(1)Pt+1(τ)|Ft]=Pt(τ+1).

对于每个t, 有无限多个集合(pjt, qjt)j∈E; t∈T满足这些条件,因此有无限多个鞅测度.

定理4 过程pt给出在等价鞅测度 P*下,期限结构在t时刻向上移动的概率,即pt=P*[ζt+1=uYt|Ft].

【证】P*[Aj,ut+1|Ft]=P*[Yt+1=j, ζt+1=uYt|Ft]=

E*[IAj,ut+1|Ft]=1/(Dt)E[IAj,ut+1Dt+1|Ft]=

E[(pjt)/(πjt)IAj,ut+1|Ft]=pjt

因为∑mj=1pjt=pt, 所以pt=P*[ζt+1=uYt|Ft].

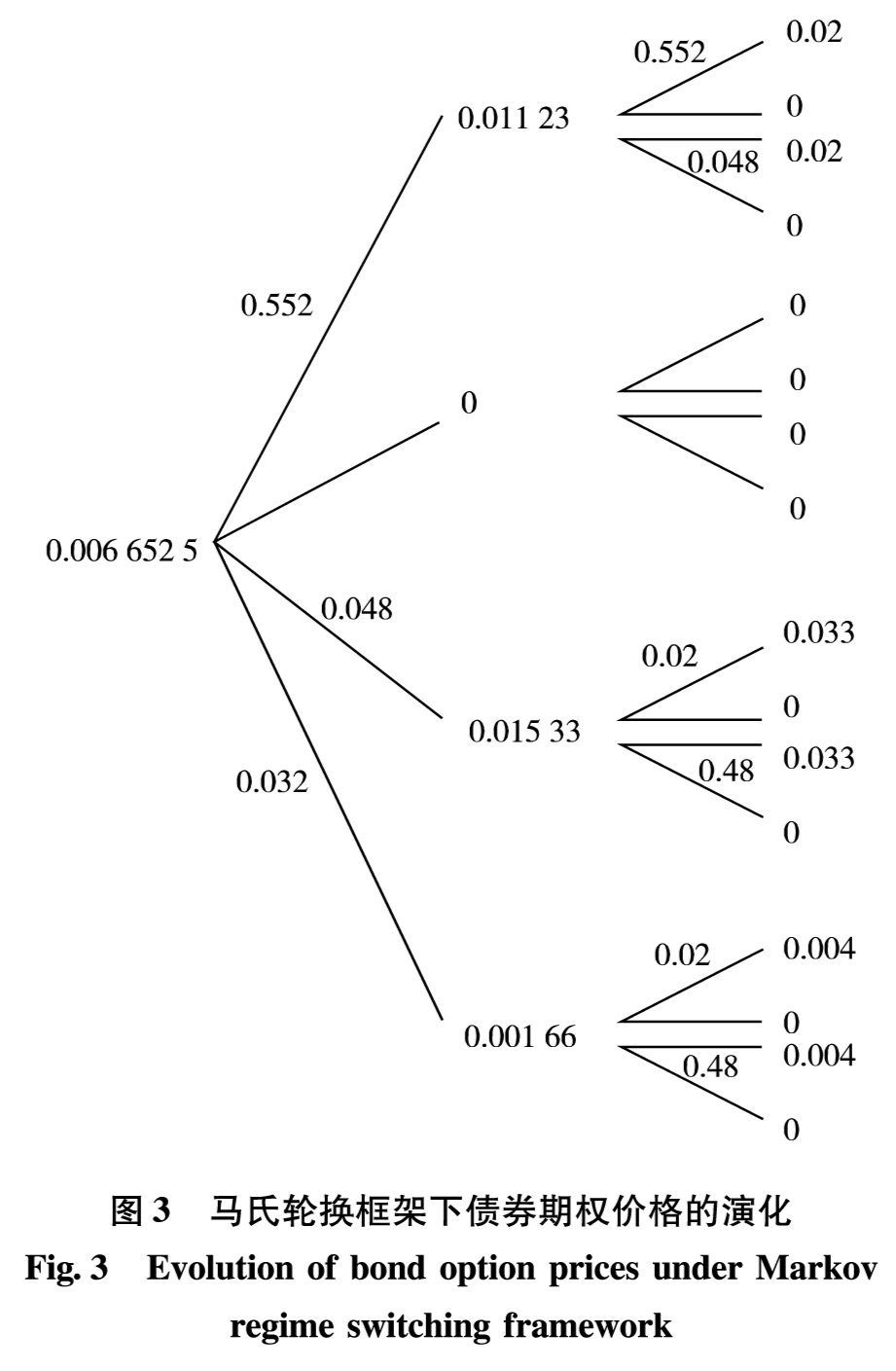

本研究采用最小熵鞅测度(minimal entropy martingale measure, MEMM)的方法确定1个风险中性轮换概率矩阵.实际上,对于不完备市场中的期权定价,MEMM是一种受欢迎的方法,其基本思想是选取一个等价的鞅测度使这个等价鞅测度和物理概率测度之间的相对熵最小,即两个概率测度之间的距离最小.

定义1 令P和 Q是两个概率测度,相对熵I(P,Q)定义为

I(P,Q)={EP[(dQ)/(dP)ln((dQ)/(dP))], QP

+∞, 其他

如果在所有等价鞅测度的集合中,测度Q使相对熵最小,则称Q为最小熵鞅测度.

由于等价鞅测度由密度过程Dt来刻画,所以刻画最小熵鞅测度等价于给出与最小熵鞅测度有关的密度过程的参数pjt和qjt.

定理5 最小熵鞅测度的特征为

pjt=vjt((1-dYt)/(uYt-dYt)); qjt=vjt((uYt-1)/(uYt-dYt)).

【证】 根据定义1,在单期模型中的目标是找到pjt和qjt(对于所有的j),使∑mj=1[pj0ln((pj0)/(πj0))+qj0ln((qj0)/(kj0))]最小,且服从约束(确保测度是1个等价鞅测度),

∑mj=1(pj0+qj0)=1; uY0∑mj=1pj0+dY0∑mj=1qj0=1(7)

这是一个有约束的最优化问题,应用拉格朗日乘数法.令

L=E[Dtln(Dt)]+λ[∑mj=1(pj0+qj0)-1]+

γ(uY0∑mj=1pj0+dY0∑mj=1qj0-1)=

∑mj=1[pj0ln((pj0)/(πj0))+qj0ln((qj0)/(kj0))]+

λ[∑mj=1(pj0+qj0)-1]+

γ[uY0∑mj=1pj0+dY0∑mj=1qj0-1]

对pj0和qj0求偏导数并令方程等于0得(对于每个j)

pj0=πj0exp[-(1+λ+γuY0)];

qj0=kj0exp[-(1+λ+γdY0)](8)

根据式(8)及对λ和γ的偏导数得

exp(-γuY0)∑mj=1πj0+exp(-γdY0)∑mj=1kj0=

exp(1+λ)(9)

uY0exp(-γuY0)∑mj=1πj0+dY0exp(-γdY0)∑mj=1kj0=

exp(1+λ)(10)

混合式(9)和式(10)得

exp(-γdY0)=

exp(-γuY0)((uY0-1)∑mj=1πj0)/((1-dY0)∑mj=1kj0)(11)

根据式(8)至式(11)以及πj0、 kj0和vj0的定义,即得pj0=vj0((1-dY0)/(uY0-dY0))、 qj0=vj0((uY0-1)/(uY0-dY0)).

在n期模型中,目标是找到pjs和qjs使得EP[(dQ)/(dP)ln(dQ)/(dP)]最小,且服从约束.对于t

∑mj=1(pjt+qjt)=1; uYt∑mj=1pjt+dYt∑mj=1qjt=1; qjt, pjt>0.

由归纳法得拉格朗日乘数的表达式为

L=∑n-1i=0{∑mj=0[pjiln((pji)/(πji))+qjiln((qji)/(kji))]+λi[∑mj=1(pji+qji)-1]+γi[uYi∑mj=1pji+dYi∑mj=1qji-1]}

令拉格朗日乘数L对pi、 qi、 ri和λi(对每个i)求偏导,并令方程等于0.用与单期模型相同的方法混合所有方程,即得pjt=vjt((1-dYt)/(uYt-dYt))、 qjt=vjt((uYt-1)/(uYt-dYt)). 显然结果满足正定性.

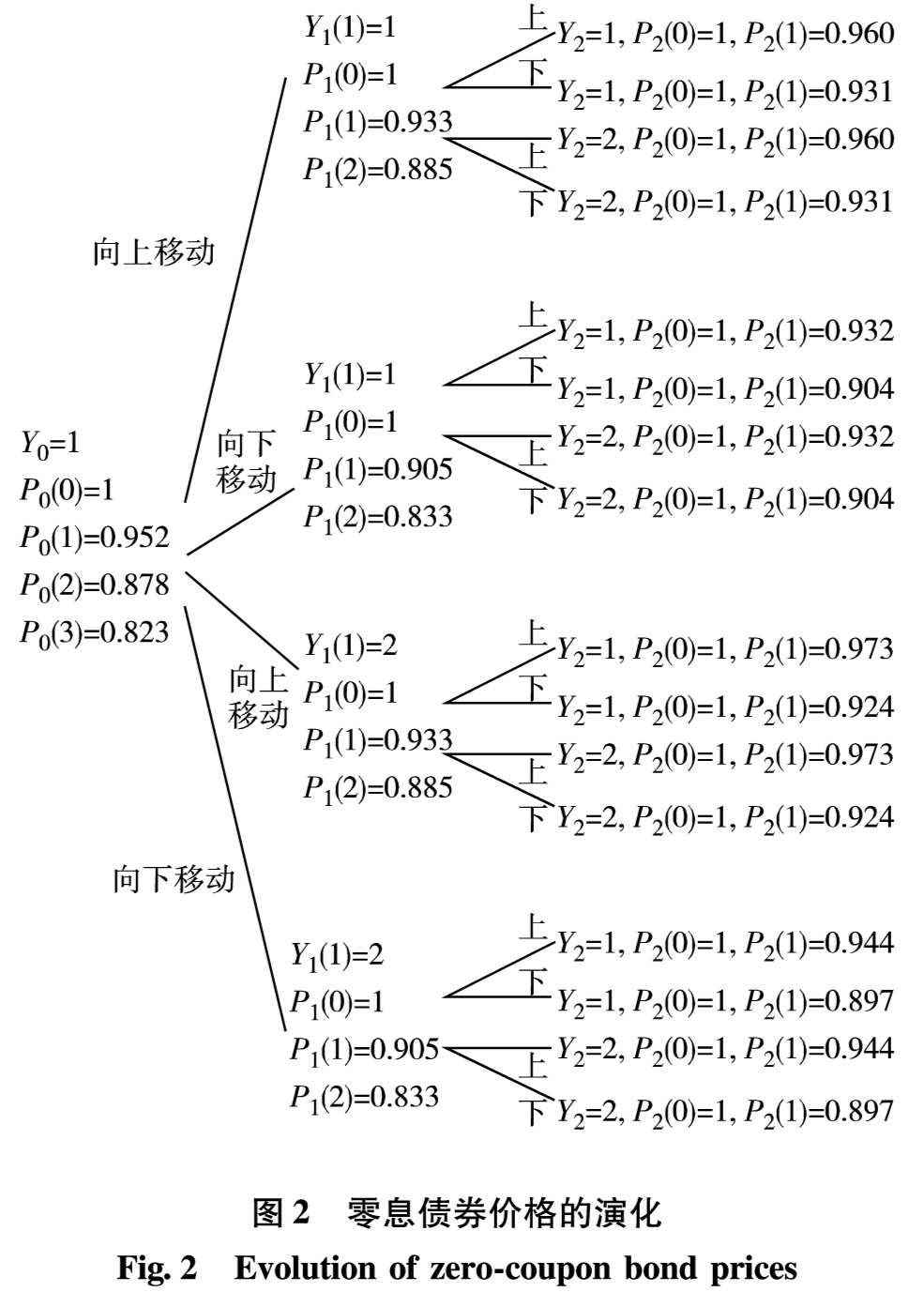

1.5 二叉树模型的拓展

经典Ho-Lee模型构造的二叉树期权定价中,假设零息债券的价格函数从1个状态到另1个状态的演化只依赖向上运动的数量,不依赖发生的顺序.根据路径独立性得到向上和向下参数的明确表达式.本节旨在讨论市道轮换下的路径独立性.

定理6 假设给定Ft和价格为Pt(τ+2)的零息债券.下面考虑AYt,ut+1、 AYt,dt+2和AYt,dt+1、 AYt,ut+2两条路径. 若施加条件两条路径零息债券的价格相同,则存在一个常数δYt, 使得

uYt(τ)=1/(pYt+(1-pYt)δτYt)

dYt(τ)=δτYtuYt(τ)

【证】 对于第1条路径有

Pt+2(τ)=(dYt(τ)uYt(τ+1)Pt(τ+2))/(uYt(1)Pt(2)); 对于第2条路径有Pt+2(τ)=(uYt(τ)dYt(τ+1)Pt(τ+2))/(dYt(1)Pt(2)).

令上述两式相等得

(dYt(τ)uYt(τ+1))/(uYt(1))=(uYt(τ)dYt(τ+1))/(dYt(1))(12)

根据式(4)有dYt(τ)=(1-pYtuYt(τ))/(1-pYt), 代入式(12)得

(1-pYtuYt(1))/(uYt(1)-pYtuYt(1))·(1-pYtuYt(τ))/(uYt(τ))=

(1-pYtuYt(τ+1))/(uYt(τ+1))(13)

此结果恰好类似经典的Ho-Lee模型.定义

δYt=(1-pYtuYt(1))/(uYt(1)-pYtuYt(1))(14)

将式(14)代入式(13)得1个简单的差分方程.已知uYt(0)=1, 用迭代法得uYt和dYt的解

uYt(τ)=1/(pYt+(1-pYt)δτYt)

dYt(τ)=δτYtuYt(τ)(15)

由式(15)可知,对于每个可能的状态Yt, 若给定δ'Yts(对于每个状态是一个常数)和p'Yts(状态Yt时向上或向下移动的概率),则整个期限结构被完整的定义.这个模型除了需要选取可能的状态外,与Ho-Lee模型相同.定理6在状态不变时,应用路径独立性得到了uYt(τ)和 dYt(τ)的明确表达式.推论2将在状态发生变化的条件下研究路径独立性的思想.

推论2 为简化记号,令Yt=i. 假设存在价格为Pt(τ+3)的零息债券, Aj,dt+1, Ai,dt+2, Ai,ut+3和Ai,ut+1, Aj,dt+2, Ai,dt+3有两条路径.应用路径独立性得到1个联立方程(对于每个τ):

f(pj)=0

f(pj)=p2j(1-δj)(1-δτj)(pi+(1-pi)δτ+1i)+

pj{δτ+1j[δτ+1i(pi-1)(pi+1)-

δi(1-pi)pi(δτ+1i+1)+pi(pi-2)]+

δτj[pi+δτ+1i(1-pi)]+

δj[pi+δτ+1i(1-pi)]-[pi+

δτi(1-pi)][pi+δi(1-pi)]}+

δτ+1jpi(1-pi)(1-δi)(1-δτi)(16)

【证】 将模型用于第1条路径得

Pt+3(τ)=(dj(τ)di(τ+1)ui(τ+2)Pt(τ+3))/(di(1)ui(2)Pt(3))

将模型用于第2条路径得

Pt+3(τ)=

(ui(τ)dj(τ+1)di(τ+2)Pt(τ+3))/(dj(1)di(2)Pt(3)).

令上述两式相等得

(ui(τ)dj(τ+1)di(τ+2))/(dj(1)di(2))=

(dj(τ)di(τ+1)ui(τ+2))/(di(1)ui(2))

根据di(τ)=δτiui(τ)(对于uj和dj此式也成立),且分离i项与j项得

(ui(τ)ui(1))/(ui(τ+1))=(dj(τ)dj(1))/(dj(τ+1))(17)

根据式(15)得式(18),其对每个τ都成立

[p2j+pj(1-pj)δj+pj(1-pj)δτj+

(1-pj)2δτ+1j][pi+(1-pi)δτ+1i]=

[pj+(1-pj)δτ+1j][p2i+pi(1-pi)δi+

pi(1-pi)δτi+(1-pi)2δτ+1i](18)

重新排序各项即得期望的结果.

如果固定pi、 δi和δj, 方程(16)得到一个关于pj的二次方程系统(对于每个τ).因为给定的这些方程的系数依赖于τ, 所以它们是不相同的.一个解pj∈(0,1)是否能同时解出所有方程尚不清楚.那么是否可以找到一个条件,使得在这个条件下,解pj∈(0,1)存在呢?下面定理可提供部分答案.

定理7 假设δi=δj, 则给定pi, 方程(16)的系统至少存在一个解pj.

【证】 固定δi=δj, 则对每个τ, 给定pi(pi∈(0,1))的任何值,都至少存在一个解pj且pj=pi, 从方程(18)可见,这是显然的.

尽管有定理7,情况仍不理想.因为在δi≠δj时,二次方程解的存在性仍不清楚.事实上,唯一保证可行的模型是pi=pj且δi=δj时的模型,此时对于所有的(i, j)和τ, 都有ui=uj且di=dj, 即期限结构在所有状态的演化都由相同的值控制,这就如同只有1种状态.总之,在市道轮换存在时,唯一保证可行的模型是每个状态的期限结构都相同的模型,然而此时整个市道轮换结构变得没有意义.为使市道轮换存在实际意义,在存在市道轮换时不能应用路径独立的条件.